Daphnée graduated at LSE with a PhD, specializing in the regulation of financial technological innovation in France.

Her research focuses on crowdfunding and crypto-asset regulation.Before embarking on her PhD, Daphnée earned her master's degrees from the LSE in European Politics & Theory and History of International Relations, as well as from Sorbonne University in European Affairs & Law.

Insights on how stablecoins are upgrading the banking stack for speed, reach, and efficiency.

In this article we explain how Kulipa can operate a card connected directly to a wallet it does not control, processing payments with no collateral whilst retaining a fast and efficient UX for users.

As the blockchain ecosystem matures, better and more diversified ways of authenticating for blockchain transactions have emerged. This can be quite overwhelming to newcomers, and so this post aims to put order in the following terms: EOA/ MPC/ Account abstraction/ Paymaster/ Relay/ Key abstraction

.avif)

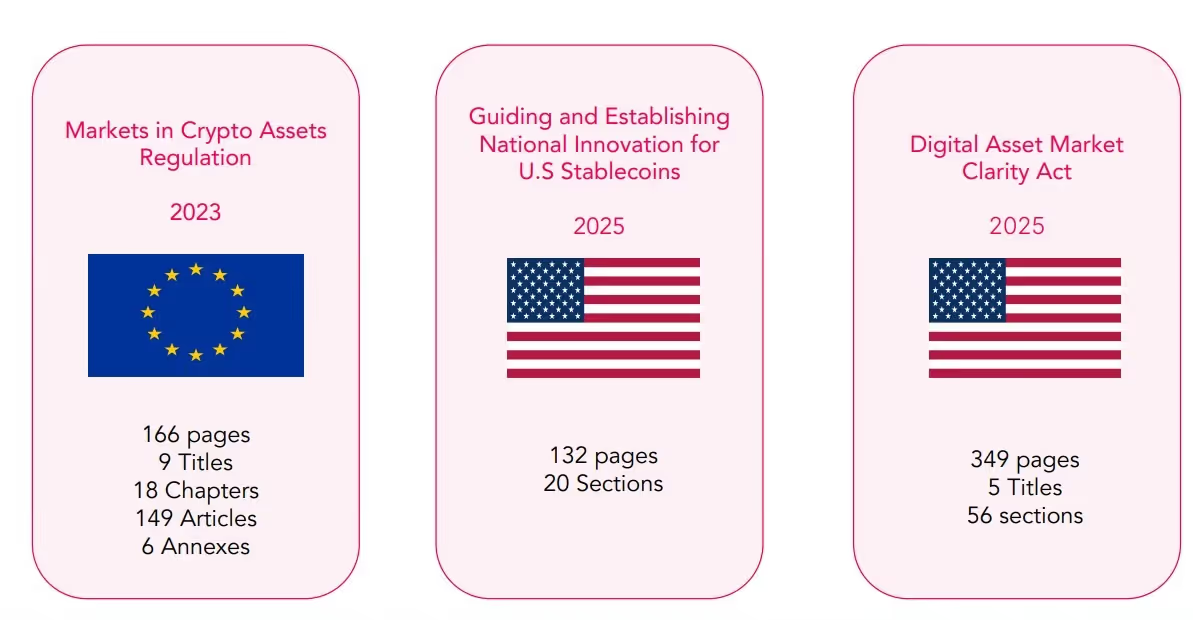

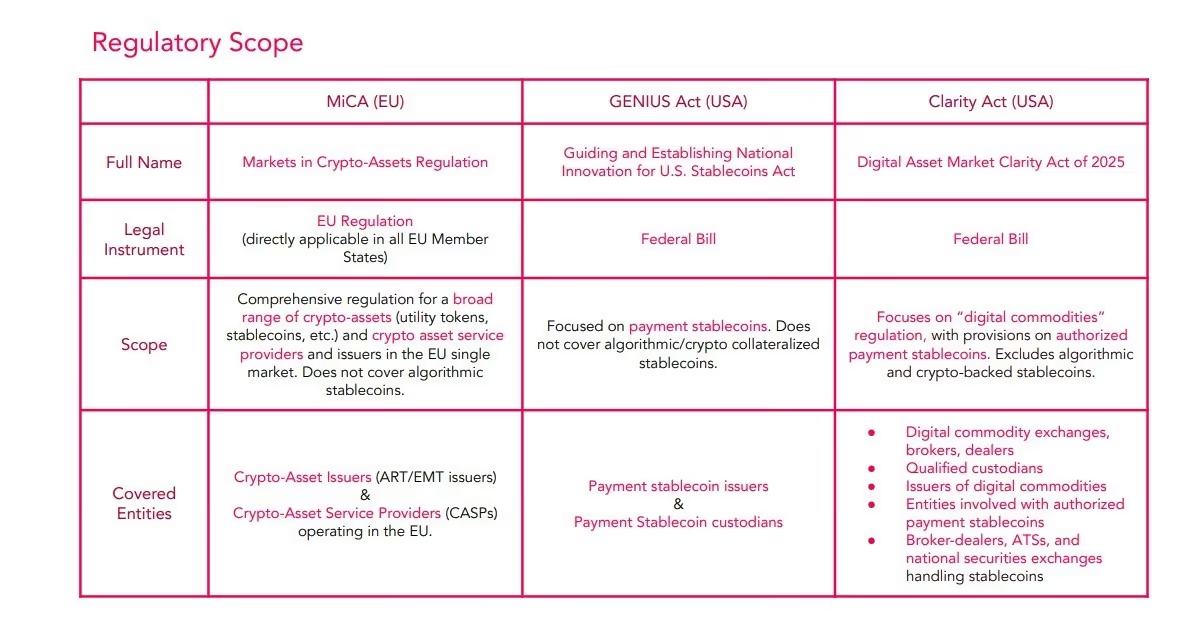

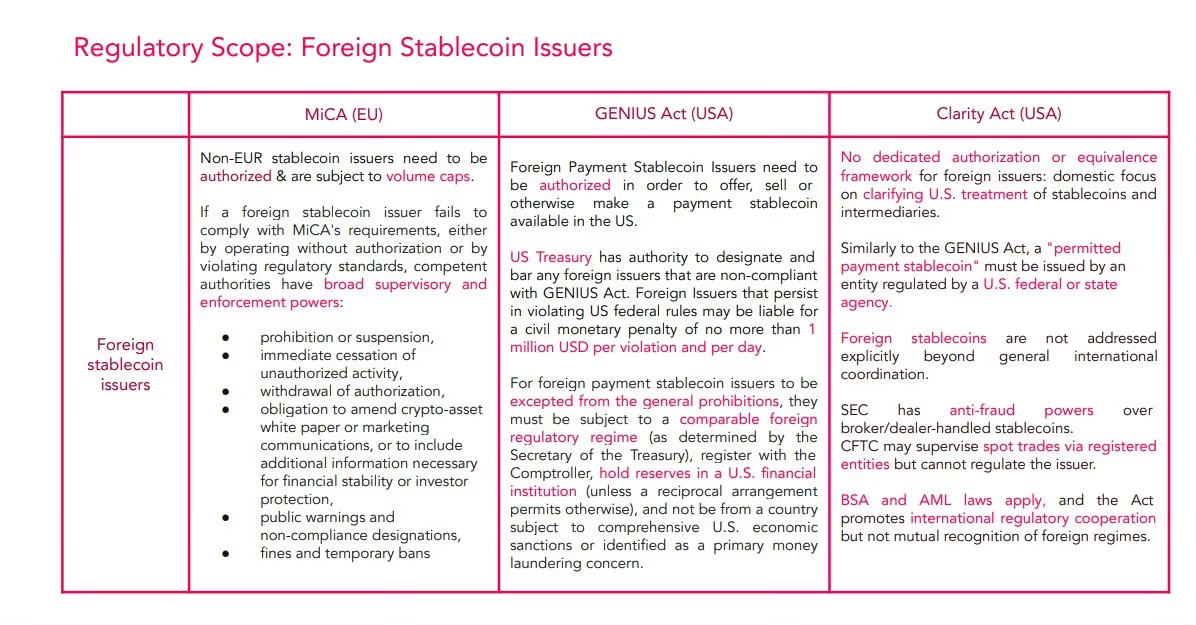

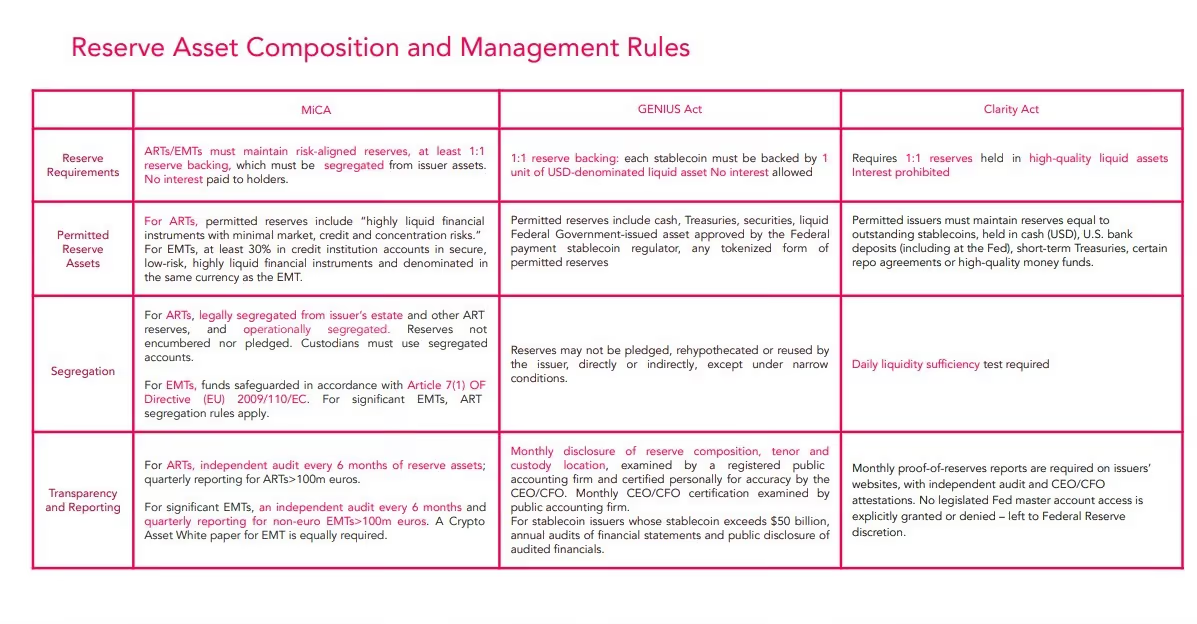

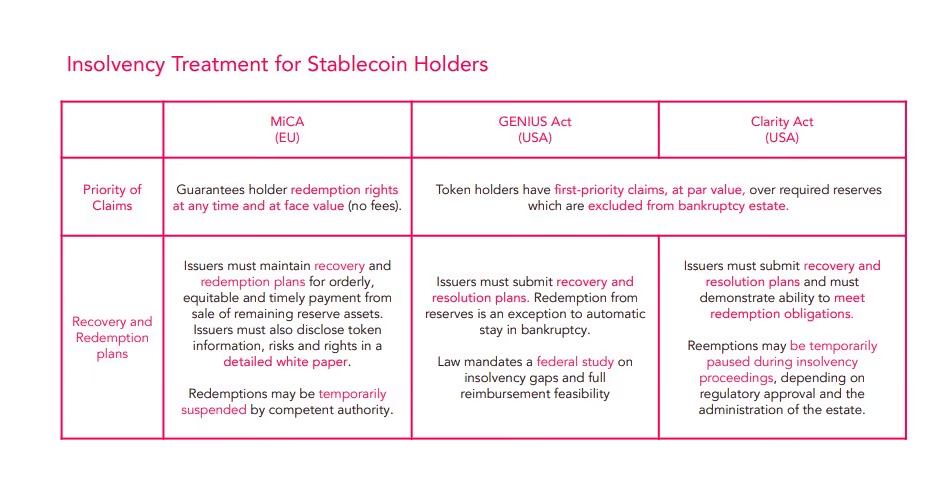

Welcome to Kulipa's Regulatory Radar #4! In this Regulatory Radar, the third of our dedicated series on US digital asset developments, we delve into reactions of key EU institutions - ECB, EC, and EP - following the landmark vote of the GENIUS Act.

Welcome to Kulipa's Second Regulatory Radar! In this Regulatory Radar, the first of a new dedicated series, we explore the evolving legislative journey of the GENIUS Act—Guiding and Establishing National Innovation for US Stablecoins Act—a landmark bill designed to create a comprehensive regulatory framework for payment stablecoins in the United States.

Stablecoin infrastructure is faster and cheaper, and companies are using it to fundamentally rebuild payment infrastructure for the next decade of financial services. The great fintech migration isn't coming. It's here.

On 10 June 2025, the European Banking Authority (EBA) issued a no-action letter addressing the interaction between PSD2 and MiCA—marking the first time this tool has been used to navigate the complex overlap between legacy payments regulation and Europe’s new crypto framework. But what exactly is a no-action letter in the EU context? Who can issue one? What’s its legal weight? And why should market participants and policymakers alike pay attention? Let’s take a closer look.

Fed Governor Powel Pushes for Stablecoin Regulation, Tether Invests in Zengo Wallet, Klarna Explores Crypto Integration Ahead of IPO

SEC Shifts Crypto Enforcement Strategy, Sen. Hagerty to Introduce Stablecoin Bill, Stablecoin Market Cap Surges to $200B

ECB Pushes for Digital Euro Amid US Policy Changes, Binance Faces French Money Laundering Probe, Andreessen Horowitz Exits UK for US Focus

Trump nominates the SEC and CFTC Commissioners, Circle acquires Hasnote, ESMA pushes for eelisting of non-MiCA compliant stablecoins

Coinbase Launches Bitcoin-Backed Loans, first signs of Trump's decisions to come, more and more banks exploring crypto, regulatory clarity coming to Kenya

CFTC Chair Warns of Crypto Gaps, Venezuelans Ditching Dollars for Crypto, Bhutan adds crypto to strategic reserves

Bitcoin reserves on the agenda of a lot of governments, second largest French bank to offer crypto, MoonPay acquiring Helio Pay

Ripple finally launches RLUSD, India advocates global crypto regulation framework, MiCA-compliant stablecoins dominate European markets, Usual Adopts M0 Infrastructure for Stablecoin

Circle and Binance Partner to Boost USDC Adoption, Stablecoin Market Cap Nears $200 Billion, Digital Euro Leader Resigns Amid Controversy, India's Central Bank Sees CBDC Potential

David Marcus stance on the death of Diem (formerly Libra), Nuvei Expands Blockchain Payments in Latam, Coinbase Exec Predicts Stablecoin Regulations in the US by 2025

Robinhood Adds USDC in EU Markets, BlackRock-Backed Stablecoin Gains Traction, Coinbase Won't Support Celo Migration

In previous articles, we’ve detailed how payments work, noting that the incentive for much of the work done by various players is being able to receive a portion of the interchange fees. Today, we’ll go into more detail on the interchange fee, including who shares it, how it’s calculated, and why Kulipa brings clarity to its partner wallets about what they’ll earn.

US SEC Chair, Gary Gensler Stepping Down in January 2025; Paxos Seeks EU Market Access with Membrane Finance acquisition; Tether launching MiCA-compliant stablecoins with Kraken and Quantoz Payments

USDT Crude Oil Transaction, Sling enters the US, Underbanked US Households Rely on Crypto

French Gambling Regulator May Ban Polymarket, JPMorgan Expands Blockchain FX Settlements, Seven South Korean Banks Join CBDC Pilot, Helio Expands Solana Payments on Shopify

Paxos launches USDG, Ant CEO praises tokenization, Tether's dirham-pegged stablecoin launch, U.S. Treasury notes stablecoin influence on T-bills

.avif)

85% of traded volumes happen off-chain, on CEXs. The problem is that CEXs are custodial, and not interoperable like on-chain protocol. And as these centralised solutions offer a better UX than their decentralised counterparts, it's easy to think that crypto might just become another commodity just good enough to be traded for profits, in neobanks-like structure. In short: is web3 devolving back into web2? That's what we're exploring today in this new Deep Dive rant.

Stripe Acquires Bridge, Avalanche and Visa’s New Crypto Card, Argentina full support to crypto and more regulatory updates

Stripe's Strategic Expansion in Stablecoins with Paxos and Bridge, Stablecoin Adoption: US Lags, EU Gains Momentum, Ripple Expands Global Reach with RLUSD Stablecoin

In our previous article, we explained the criteria for determining if your wallet would be best served by a debit card or a prepaid card. As mentioned, the smooth user experience offered by crypto debit cards comes with some additional technical issues; below, we detail how Kulipa handles them based on account characteristics, security keys, risk management, and more.

.avif)

Coinbase Delisting Stablecoins, Paxos yield-generating stablecoin, Stripe’s Return to Crypto Payments...

Choosing between prepaid and debit crypto cards is a crucial decision for wallets looking to enhance user experience and drive engagement. This article explores the key differences between the two, to help wallets determine the best fit for their growth strategy.

SWIFT, PayPal, and Ripple Deepen Engagement in Crypto Payments, LatAm and Asian government continue to push for crypto, ECB and Börse Stuttgart projects in crypto...

Robinwood and Revolut exploring stablecoin issuance while Visa launches a stabelcoin issuance platform for banks, Crypto booming in Bolivia after its legalization...

Are embedded wallets the key to mainstream stablecoin adoption? In this interview with Mathilde David, Product Lead for Stablecoin Movement at Paxos, we explore how user-friendly Web2 wallets could simplify crypto payments. Learn about the regulatory challenges, payment innovations, and opportunities shaping the future of stablecoins in this ever evolving financial landscape.

Circle improving their service in LatAm, Soneium already getting the USDC, crypto recognized as property in the UK, JPMorgan doubles down on crypto

This article breaks down the payment authorization and settlement processes, and explores how crypto debit cards function by leveraging existing financial infrastructure. It also explains how Kulipa enables wallets to issue branded crypto cards that work seamlessly with Visa and Mastercard networks.

.avif)

Report by Visa on real world use cases for stablecoin, UK recognizes crypto as personal property, regulatory clarity enabling geographical expansion globally

Nigeria SEC issuing the first crypto licences, 87% of crypto licences application fail, a CBDC pilot in Brazil, DWF synthetic stablecoins to launch soon and much more...

This week in our Compass: Tether drops its own chain project, Binance embraces a MiCA compliant stablecoin, Japan and Hong Kong confirm their commitment to crypto, and more...

This week in our Compass: Binance still under regulatory pressure despite it effort, EURC coming to Europe with Coinbase, Tether launching a Dirham stablecoin, Quidax first licensed exchange in Nigeria, and much more...

This three weeks in our Compass: Contrasted Regulatory Evolutions (India, France, Brazil...), Metamask officially announcing their card, new promising stablecoins, and more...

.avif)

This week in our Compass: finally the launch of the first US ETH ETFs, 3 CBDC projects accros the globe, first company capitalised in crypto in Argentina

This week in our Compass: Stripe enabling card on-ramp for their EU merchants, Blackrock CEO legitimising Bitcoin and a busy summer for regulators

Today, we’re excited to announce the launch of the first zk-powered debit card for seamless stablecoin spending, in partnership with Argent, and backed by $3 million in funding. This marks a significant step towards our mission of making self-custodial wallets a mainstream financial tool.

.avif)

This week in our Compass: Argent announces at crypto debit card powered by Kulipa, SEC drops its case against BUSD and a lot more announcements

.avif)

This week in our Compass: Circle becomes an EMI under MiCA and more regulatory updates from Singapore, Nigeria...

.avif)

This week in our Compass: Coinbase-Stripe partnership, Nigeria pushing a new regulation, and much more

.avif)

This week in our Compass: The SEC drops charges against Ethereum, the subtle equilibrium of stablecoins and CBDCs

.avif)

This week in our Compass: Emerging market crypto push, CBDC for x-border in Saudi and regulatory updates across the globe.

.avif)

This week in our Compass: Regulatory update in Hong Kong, EU and Rwanda, Growing crypto interest in Australia and Thailand, and consolidations in the industry

.avif)

This week in our Compass: Growth of stablecoins in Russia and PYUSD on Solana, New institutional tokenisation projects and CBDC updates in China and Israel

.avif)

This week in our Compass: Ethereum ETFs finally approved in the US, new algorithmic stablecoins and more regulatory updates

.avif)

This week in our Compass: Regulatory update from the USA, Nigeria, India and more, new stablecoin and RWA project & an update by Mastercard, some signs of challenges for the digital Yuan, and much more.

.avif)

We're thrilled to announce that Kulipa will join Mastercard's Start Path program to explore how blockchain technology can revolutionize the financial system, creating a more efficient and inclusive experience for millions around the world.

.avif)

This week in our Compass: Update on the situation in Nigeria, Ripple's stablecoin and much more

Global growth of stablecoin, CBDC projects between Iran and Russia and many more regulatory evolutions.

In this week's episode of the Deep Dive, we explore the keys to achieving the delicate balance between simplicity and security in wallet design, with Alexandre Gabadou from The Big Whale, France's leading Web3 media outlet.

.avif)

Stripe reaccepting crypto, EU voting AML regulations, 98% of countries exploring CBDCs, US bill on stablecoin and more crypto news.

.avif)

This week in crypto: CBDC race is on, self-custody and stablecoin on the rise and a regulatory update.

.avif)

This week in crypto: SEC going after DeFi, suing Uniswap, plus other updates about PYUSD, and updates from Thailand, Paraguay.

This week, we sat with Arthur Pfalzgraf, Product Manager at Ultimate Wallet for an insightful talk about the challenges that wallets face today, and how following trends ultimately hurts adoption.

.avif)

This week in crypto: Regulatory updates from Singapore, Lithuania, France and Argentina. Ripple's cash-equivalent stablecoin

On this week's episode of the Deep Dive, we explore the differences between EOA and Account Abstraction wallets, before having a look at concrete use cases for AA today.

.avif)

This week in crypto: Regulations are catching up (Estonia, EU, US) with a focus on AML compliance. Central Bank Digital Currencies (CBDCs) are gaining traction (IMF, SWIFT, UAE). Traditional finance is embracing blockchain (HSBC, UK), but challenges remain.

.avif)

This week in crypto: Central banks ramp up CBDC efforts with Hong Kong's e-HKD pilot and Liberia's partnership. Stablecoins see potential regulation relief with positive US comments but face rising competition. Regulatory focus intensifies with the UK's FCA and Argentina tightening their grip on crypto exchanges. The SEC's Ethereum probe adds uncertainty to the market.

This episode dives deeper into features and use cases that propel non-custodial wallets towards mainstream adoption. We'll explore 2 distinct use cases (remittance and integrated DeFi products) to position wallets for significant user growth and industry leadership.

In this first episode of the Deep Dive we explore non-custodial wallets features for mainstream adoption, kicking off with payments! We'll dissect seamless payment solutions and their potential to empower the vast population of unbanked adults globally.

.avif)

In this week's Crypto compass, we explore hot topics like CBDCs in Hong Kong and Israel, plus stablecoins in emerging markets and their regulation in Europe. And a lot more crypto news!

.avif)

The Philippines and Hong Kong are both testing Central Bank Digital Currencies (CBDCs). While the Philippines focuses on using CBDCs for transactions between banks and for cross-border payments, Hong Kong is exploring using their e-HKD for everyday transactions and even for tokenizing real estate assets. Even though privacy isn't the main concern here, these developments show that traditional finance is increasingly open to incorporating some aspects of cryptocurrency.

.avif)