What is the interchange fee?

You go into Starbucks and order. “That’ll be $7.89,” the cashier says. (Inflation!) You tap your card, the payment is authorized, and a minute later you’re sipping your latte.

It was convenient, fast, and Starbucks was happy you paid with a card and moved along rather than fumbling in your pocket for change. But the convenience of that card payment also costs Starbucks money, a little piece of the transaction that goes to the companies making the payment system work smoothly. One key part of that cost is called the interchange fee.

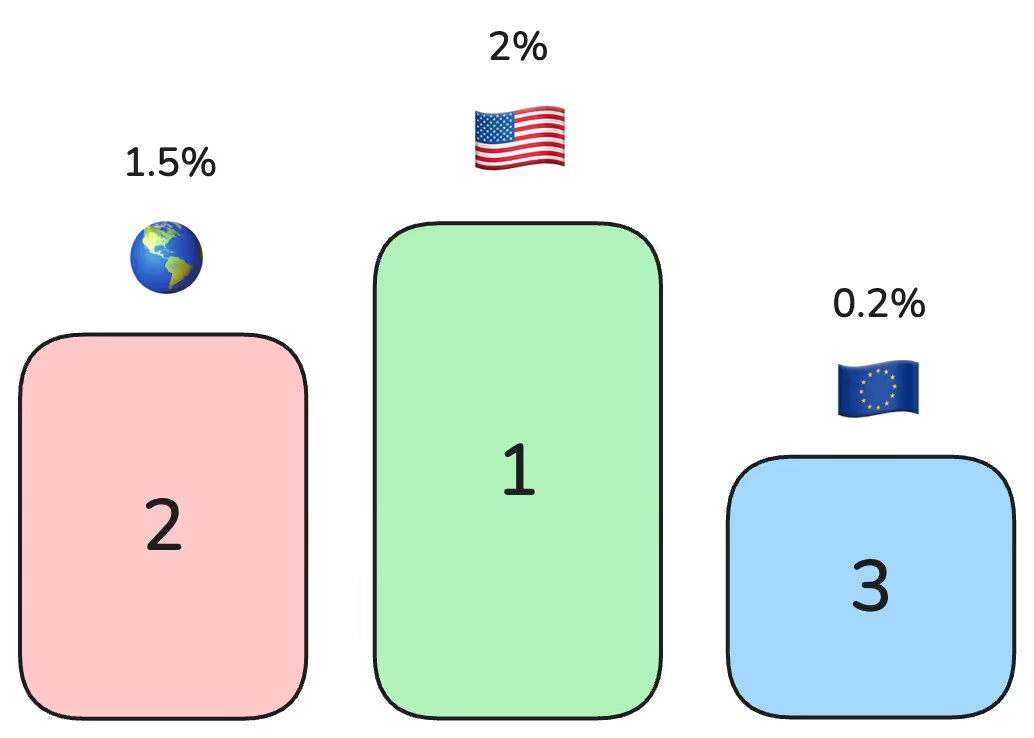

The interchange fee varies heavily depending on a variety of factors: the country in which the transaction takes place, the kind of merchant where a purchase is made (online vs. in person), whether or not it is a cross-border transaction, the type of card used (debit vs. credit, for example), and more. At Kulipa, we see that the average interchange fees on consumer purchases amount to:

- 0.2% in Europe

- 1.5% in Latin America, Africa, Asia, and the Middle East

- 2.0% in USA

In money terms, that means the interchange fees would be:

- €0.20 on €100 in France

- R$1.50 on R$100 in Brazil

- $2.00 on $100 in New York

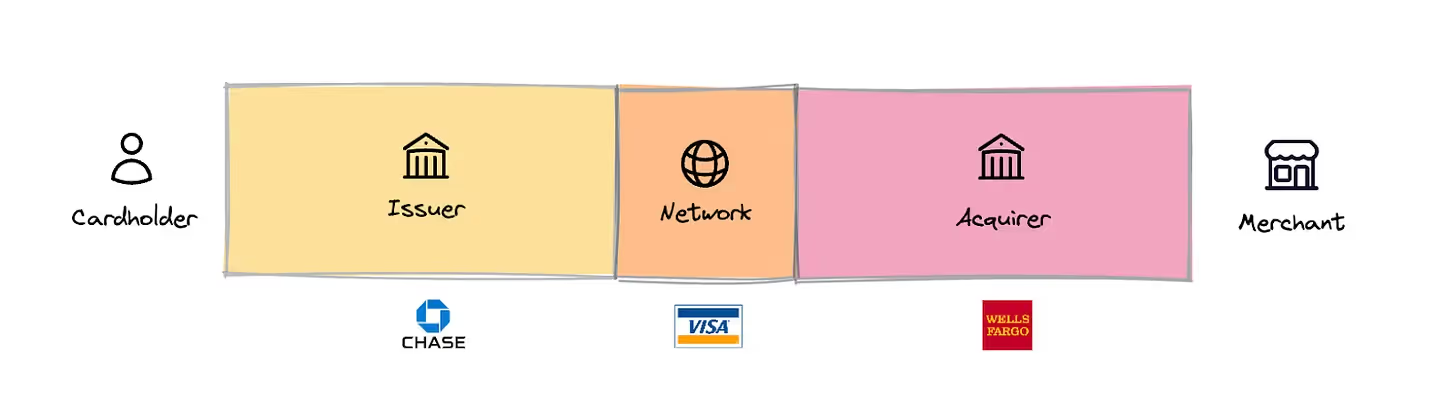

Who shares the interchange fees?

Interchange fees are divided among the different players in the transaction – with the exception of Mastercard or Visa, who have a different role that we’ll get into below.

Card issuers take the largest part of the pie in exchange for coordinating the activity among all these players. If the transaction’s card issuer has a BIN sponsor, that sponsor is also paid out of the portion of the interchange fees that goes to the issuer.

(A BIN sponsor lends their financial license to a card issuer, acting as the issuer’s guarantor with the relevant financial authorities. It is, of course, also possible that no BIN sponsor is involved if the card issuer itself has gone through the regulatory process, as for example Kulipa has done in multiple geographies.)

Interchange fees are paid by the acquirer of the transaction to the issuer (for definitions on these, check out our article on How card payments work).

How is the interchange fee calculated?

This is where Mastercard or Visa come in, as they are the ones tasked with defining and facilitating the system of interchange fees.

There’s only one place in the world where it’s quite easy to define the interchange fee: Europe. For transactions in Europe, the interchange fee is fixed by regulation for domestic transactions at 0.2% (for debit cards).

In the rest of the world, however, it’s very complicated to understand how much the interchange fee will be, today, for a given transaction happening in a given location. It can, and does, vary based on a variety of circumstances.

Final interchange fees are calculated with an Interchange Rate Designator (IRD), which is essentially a set of rules that covers pretty much any combination of potential factors to come up with the final number for a given transaction.

The range of IRDs is, frankly, wide. Here, it’s enough to say that an IRD is impacted by the type of card used, the type of merchant where the purchase is made, the geographic location of everyone involved, the technology used to complete the transaction, and the time when the transaction is submitted.

What does this all mean for a crypto wallet that issues payment cards?

Interchange fees have the potential to be an attractive new revenue stream for crypto wallets. But due to the complicated calculations involved, there’s also a certain opacity that opens the door to salesmanship in the industry.

Specifically, because it’s natural to start dreaming when thinking about the benefits of a new revenue stream, some card issuers try to sell a dream. We’ve talked with clients who have told us they were promised up to 90% of the net interchange fee on a transaction. The thing is that this flashy number is often standing in front of hidden costs, or is actually not true.

At Kulipa, our stance is that clarity and openness is better. That’s why our contracts spell out how we’ll keep somewhere between 20-50% of what we’re actually getting, depending on transaction volume, while being up front about what that number is.

That leads to one big conclusion: Wallets should be aware that while interchange fees can indeed be a great new revenue stream, they aren’t really enough to be the foundation of a thriving business. The bottom line is that payments can be a great new use case that leads to happier customers; in exchange, interchange fees are a good incentive for providing these services.

Want to learn more about how to enhance your crypto wallet with a branded debit card? Check out kulipa.xyz and reach out to set up a call to talk about your specific needs.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)