The stablecoin engine

for modern fintechs

Go global with stablecoin-backed payment products. Issue cards, open virtual accounts and move funds anywhere in seconds.

Real-time rails for

high-velocity fintechs

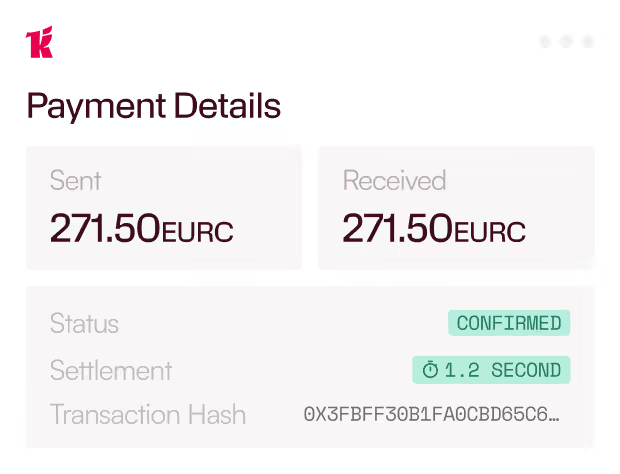

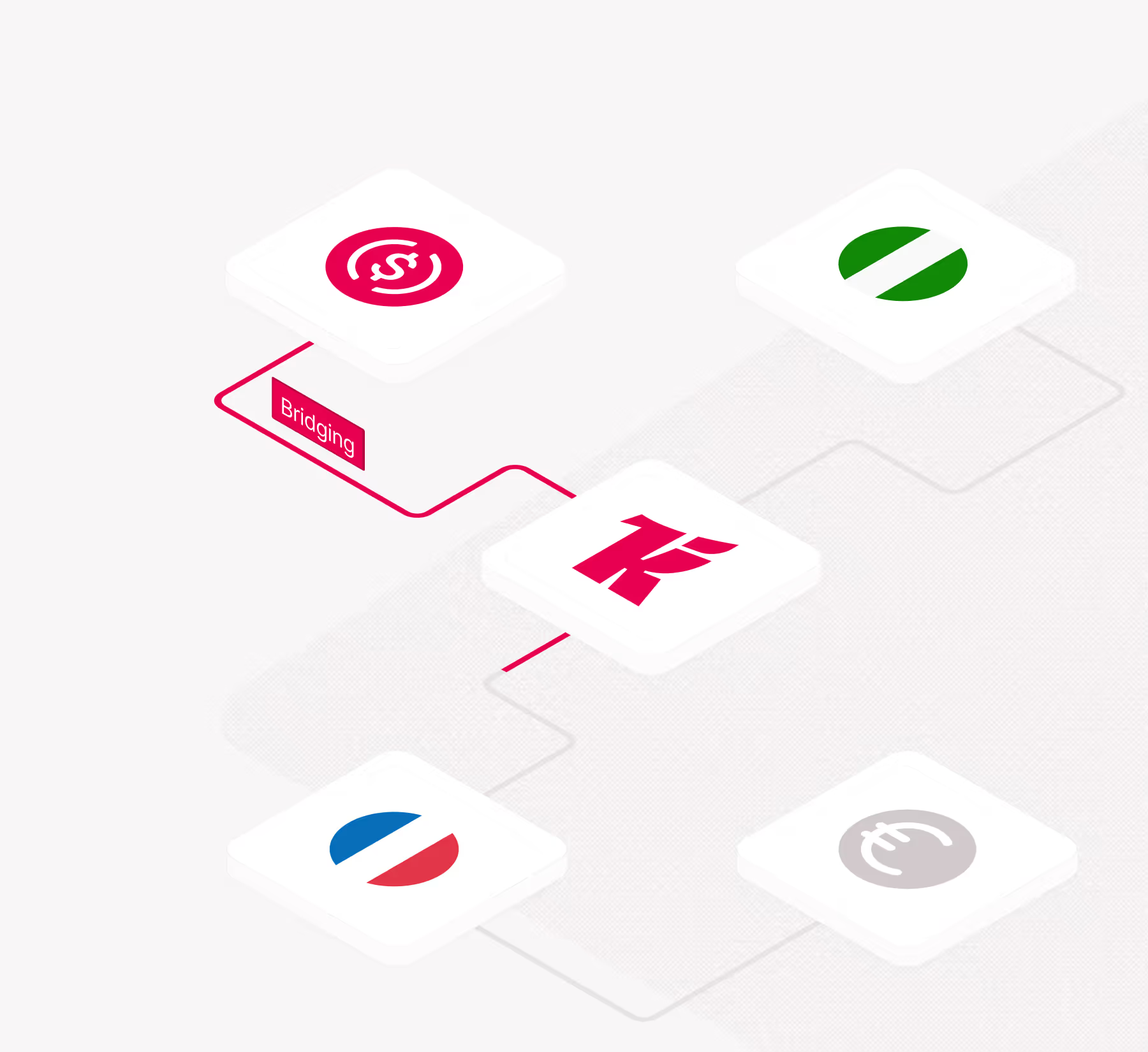

Kulipa provides the underlying infrastructure to settle global payments, manage stablecoin accounts, and issue cards - all through a unified, compliant stack.

- Grow revenue with debit cards.

- Boost acquisition with white-labelled accounts & cards.

- Scale faster with global payment products.

0

Prefunding Requirements

10x

More Cost Efficient

100+

Countries

White-labelled stablecoin products

to supercharge your fintech

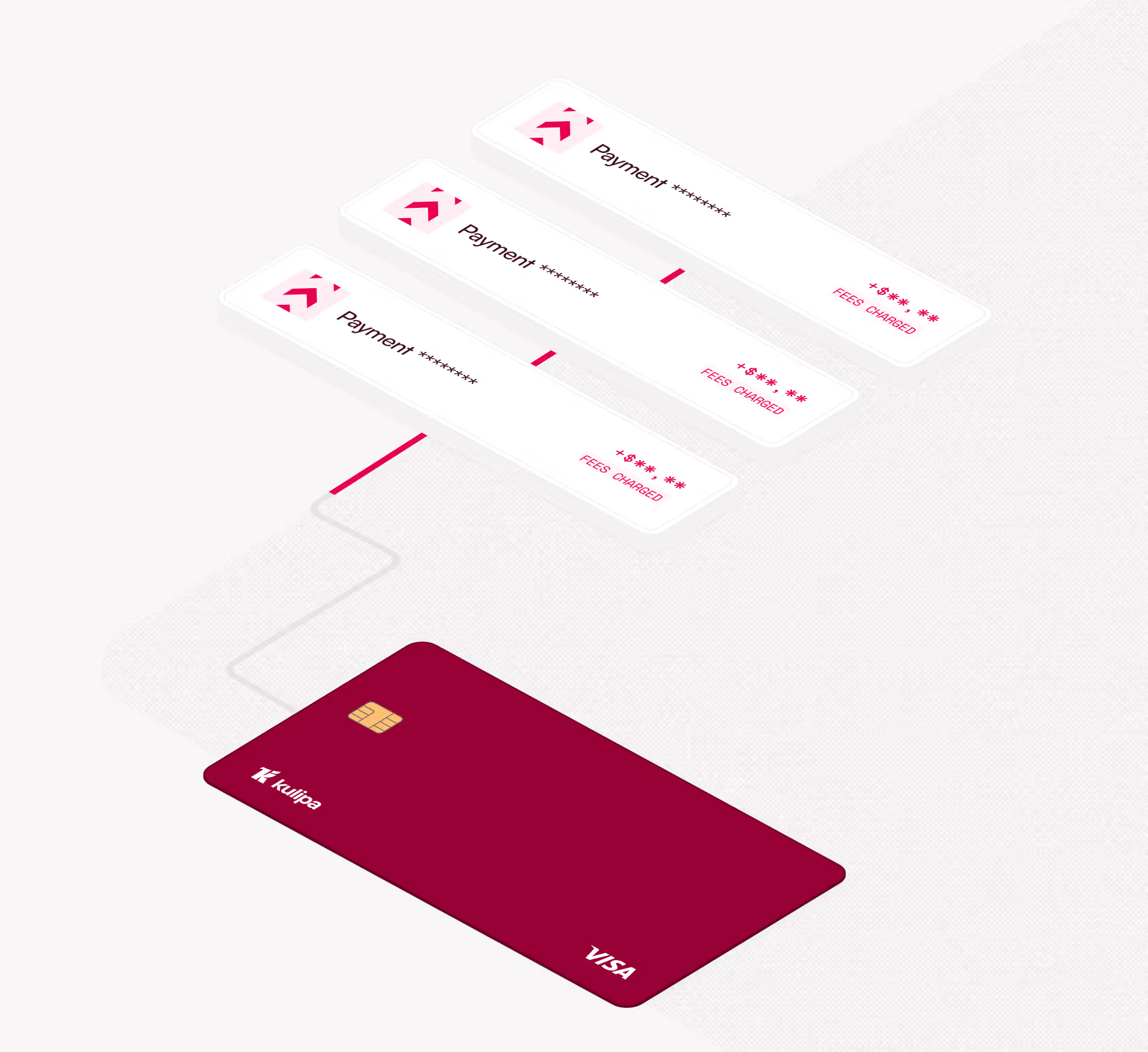

Global Card Issuance

Deploy physical and virtual cards that settle in stablecoin to the real-world. Link issuance directly to self-custody or custodial wallets to monetize interchange.

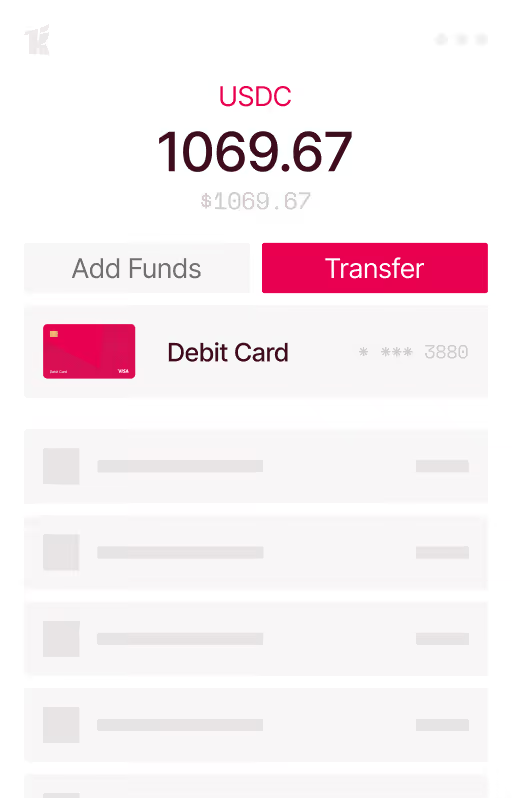

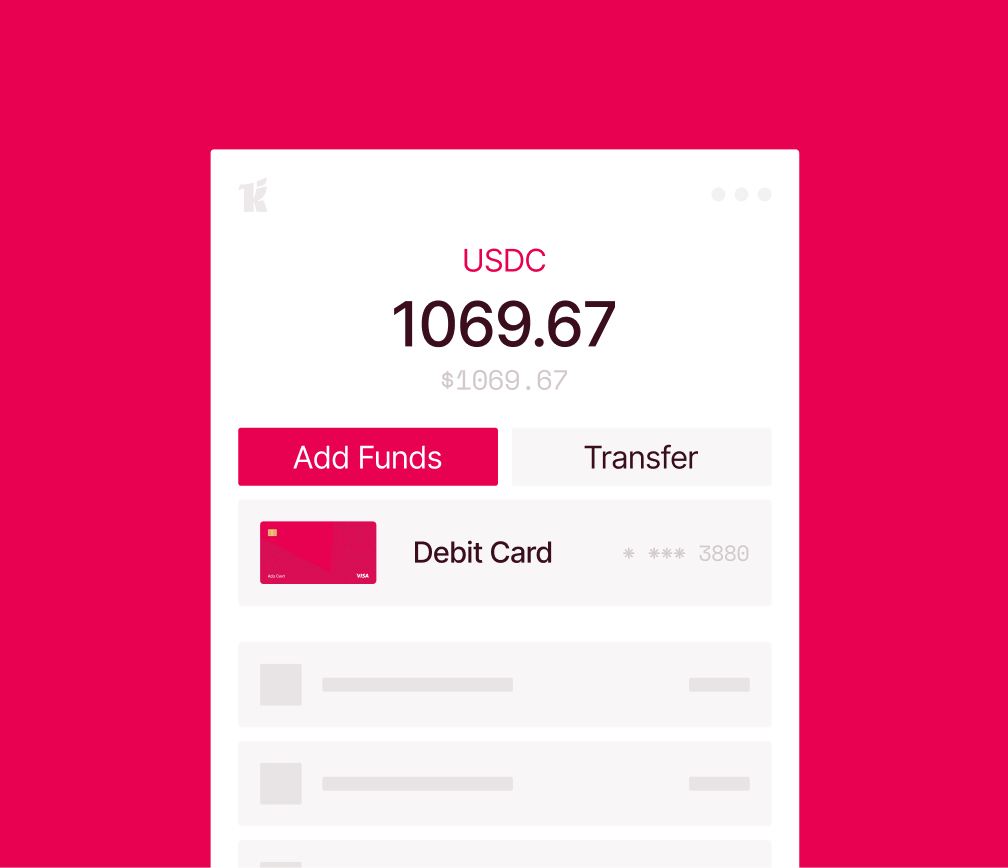

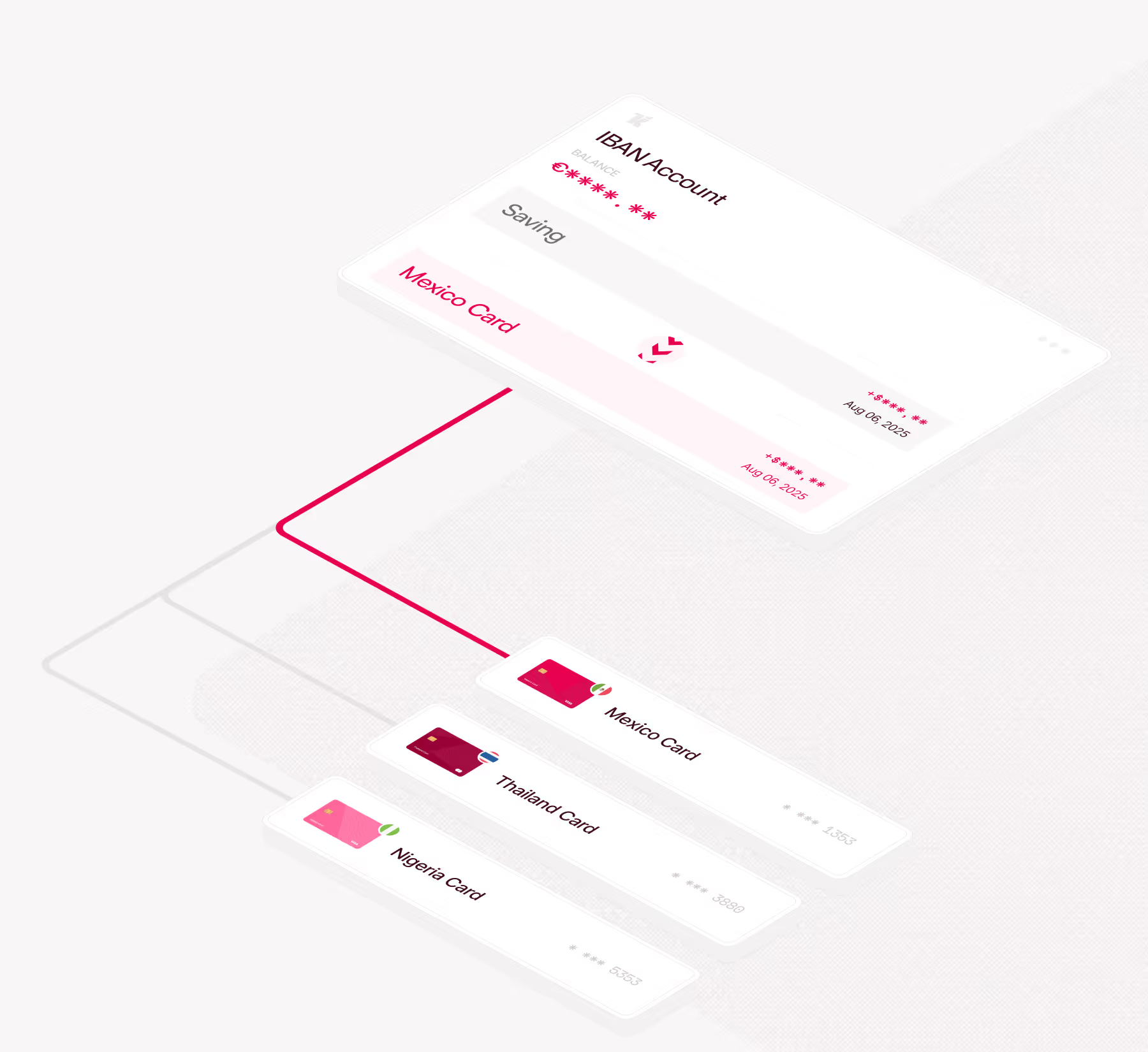

Embedded Wallet Infrastructure

Deploy famililar bank accounts UX while stablecoin rails operate in the background to handle high-speed settlements.

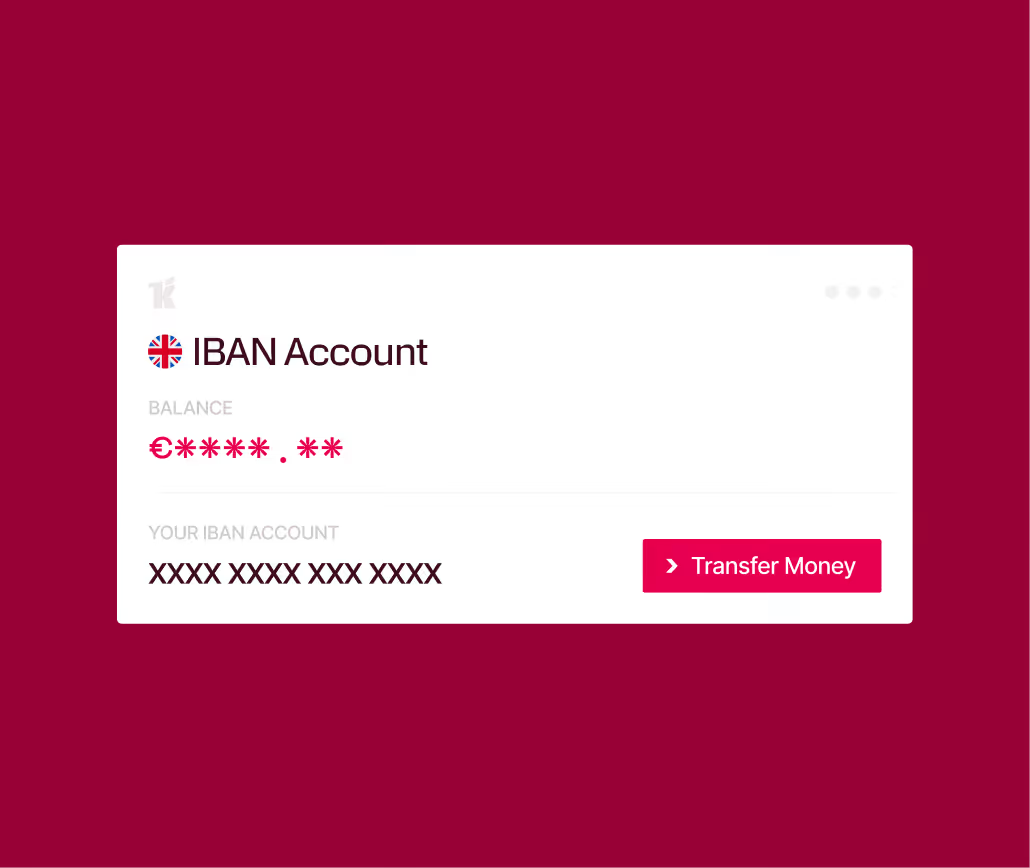

White-labelled virtual accounts

Automate seamless conversion of fiat into stablecoins, reducing the need for expensive Nostro accounts around the world.

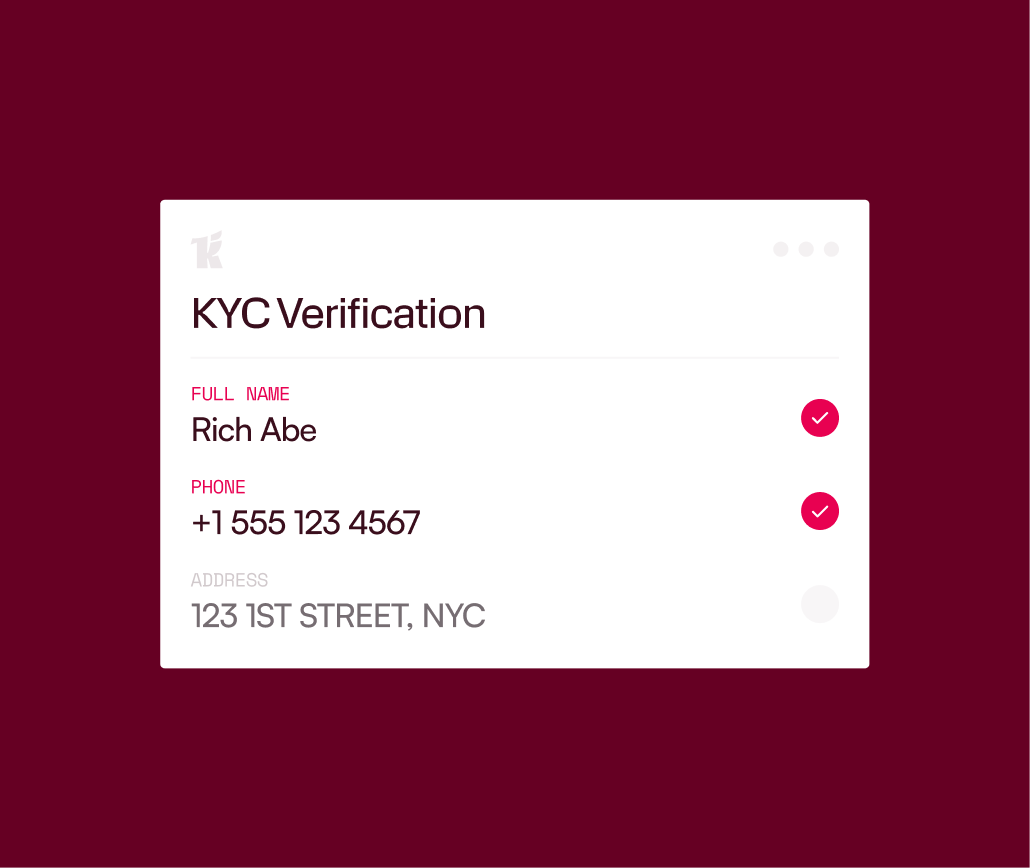

Regulatory & Compliance Shield

A full-stack compliance layer handling KYC, KYB, and AML. We provide the regulatory framework so you can launch financial products without the legal overhead.

Customer stories

Discover how leading fintechs across the world use Kulipa

“Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.”

“Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.”

“Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.”

“Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book.”

Built for

your use cases

Built for developers

Designed for scale

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Promise<void> {

const card = {

type: 'virtual',

userId: userId,

currencyCode: 'USD',

tier: 'standard',

designId: 'dsn-e8b35515-dca7-4ac4-a54c-f40c1b33ae16'

}

const headers: Headers = new Headers();

headers.set('x-api-key', 'apiKey')

const request: RequestInfo = new

Request('/cards', {

method: 'POST',

headers: headers,

body: JSON.stringify(card)

});

return fetch(request)

.then(() => {

console.log("Card issued!")

});

}

async function startKYC(userId: string):

Promise<void> {

const headers: Headers = new Headers();

headers.set('x-api-key', 'apiKey');

const request: RequestInfo = new

Request('/kyc', {

method: 'PUT',

headers: headers,

body: JSON.stringify({ userId, type: 'full' })

});

return fetch(request)

.then(() => {

console.log("KYC verification started!")

});

}

async function freezeCard(cardId: string):

Promise<void> {

const headers: Headers = new Headers();

headers.set('x-api-key', 'apiKey');

const request: RequestInfo = new

Request(`/cards/${cardId}/freeze`, {

method: 'PUT',

headers: headers,

});

return fetch(request)

.then(() => {

console.log("Card frozen successfully!")

});

}

Issue cards

Issue a virtual or physical card to any verified user - standard or premium tier, with your custom design.

Launch KYC verification

Trigger a fully compliant KYC flow for any user before issuing their first card.

Freeze a card instantly

Instantly freeze a compromised card the moment your user reports suspicious activity.

Integrate Kulipa APIs in weeks.

Go live quickly with our simple, streamlined API stack, or build the perfect user experience with our custom solutions.

Create the perfect UX

Just because you're building on stablecoins doesn't mean you should settle for sub-par UX. Build delightful payment experience, boosting retention.

Go global with top-notch security

Our out-of-the-box product suite helps you launch compliantly worldwide with bank-grade security toolings.

Boost acquisition, retention & revenue

Build delightful, end-to-end payment experiences that turn your product into a market leader.

Innovating with Ready

Ready bet on Kulipa to bring state-of-the-art debit cards to their 2 million users, getting closer to bringing stablecoin benefits to a billion people worldwide.

Watch the full interview with Itamar, Ready’s CEO, to understand how Kulipa helped design their ideal crypto card product.

Got questions?

We have answers

What is Kulipa?

We’re a one-stop-shop to help fintechs issue stablecoin-backed payment products, like cards, virtual accounts and wallets.

In which countries can I issue cards?

Through our single API, you can launch physical and virtual card programs in most countries around the world. Our cards are accepted at over 150 millions merchants globally through the Visa and Mastercard networks.

Can my users spend stablecoins directly at merchants?

Yes. Your users can spend their stablecoin balances instantly. Kulipa handles the conversion to local fiat while the user’s stablecoin balance is debited.

How secure is the Kulipa infrastructure?

We employ enterprise-grade security protocols, including real-time on-chain audit trails and 24/7/365 fraud monitoring. All stablecoin assets used for transactions are all issued by regulated providers.

How fast can we go to market?

While legacy banking integrations take months or years, you can launch a compliant stablecoin payment product with Kulipa in a few weeks.

Do I need any license to work with stablecoins?

Not for cards. Kulipa acts as your compliance layer by managing VASP licensing, KYC, KYB, and AML monitoring.

If you’re going for self-custodial wallets + virtual accounts, then you don’t need any licensing either. If you’re working on a custodial model, then regular licenses apply.

What blockchains do you support?

We can deploy on any blockchain - from EVM chains to L2 or Solana, and many more.